When most people think about investing in art, they imagine walking through galleries, trusting their instincts, and perhaps hoping for the best. But what if you could approach art investment with the same analytical rigor that guides decisions in stocks, real estate, or private equity? This is where art market indices come into play, transforming what has traditionally been an opaque market into something we can measure, compare, and understand with greater clarity.

Why Art Needs Indices: Making the Invisible Visible

Think about how stock markets work for a moment. When you want to know if the American stock market is performing well, you don't need to check every single company's stock price. Instead, you look at the S&P 500 or the Dow Jones Industrial Average. These indices give you a snapshot of market health by tracking representative companies. The art market desperately needed something similar, and over the past few decades, that's exactly what has emerged.

The challenge with art has always been its uniqueness. Every painting is one-of-a-kind, unlike shares of Apple stock which are interchangeable. This makes measuring "the market" much harder. But through sophisticated methods that I'll explain shortly, researchers have found ways to track price movements across the art world, creating benchmarks that help us understand what's really happening beneath the surface.

These indices serve several crucial purposes that parallel what financial indices do, but with some interesting twists unique to art. First and most obviously, they let us measure historical performance. Imagine you're considering investing in contemporary art versus impressionist paintings. An index can show you that over the past twenty-five years, contemporary and post-war art has significantly outperformed older periods. That's not a guarantee of future results, but it's certainly better than guessing blindly.

Second, indices allow meaningful comparisons across different asset classes. The Mei Moses index, now operated by Sotheby's, has compiled data from thousands of art sales stretching back to the nineteenth century. What it reveals is fascinating: over the last decade, art has significantly outperformed the stock market, while over a fifty-year horizon, art's average annual return of approximately 9.2% closely mirrors the S&P 500's 9.7%, though art exhibits higher volatility and lower liquidity. This kind of comparison helps investors understand where art fits in their overall wealth strategy.

Third, and perhaps most practically useful, indices help identify market cycles. Just as stock markets have bull runs and corrections, so does art. The indices reveal euphoric periods like the 1980s bubble in impressionist art or the contemporary art boom of the mid-2000s, followed by sharp contractions such as the dramatic drop in 2009 after the financial crisis. Recognizing these patterns helps investors avoid buying at peaks and potentially identify opportunities in downturns.

The Major Player Indices: Understanding Different Approaches

Let me introduce you to the main indices you'll encounter, starting with what I consider the most important for serious collectors.

The Artprice100: Art's Answer to the S&P 500

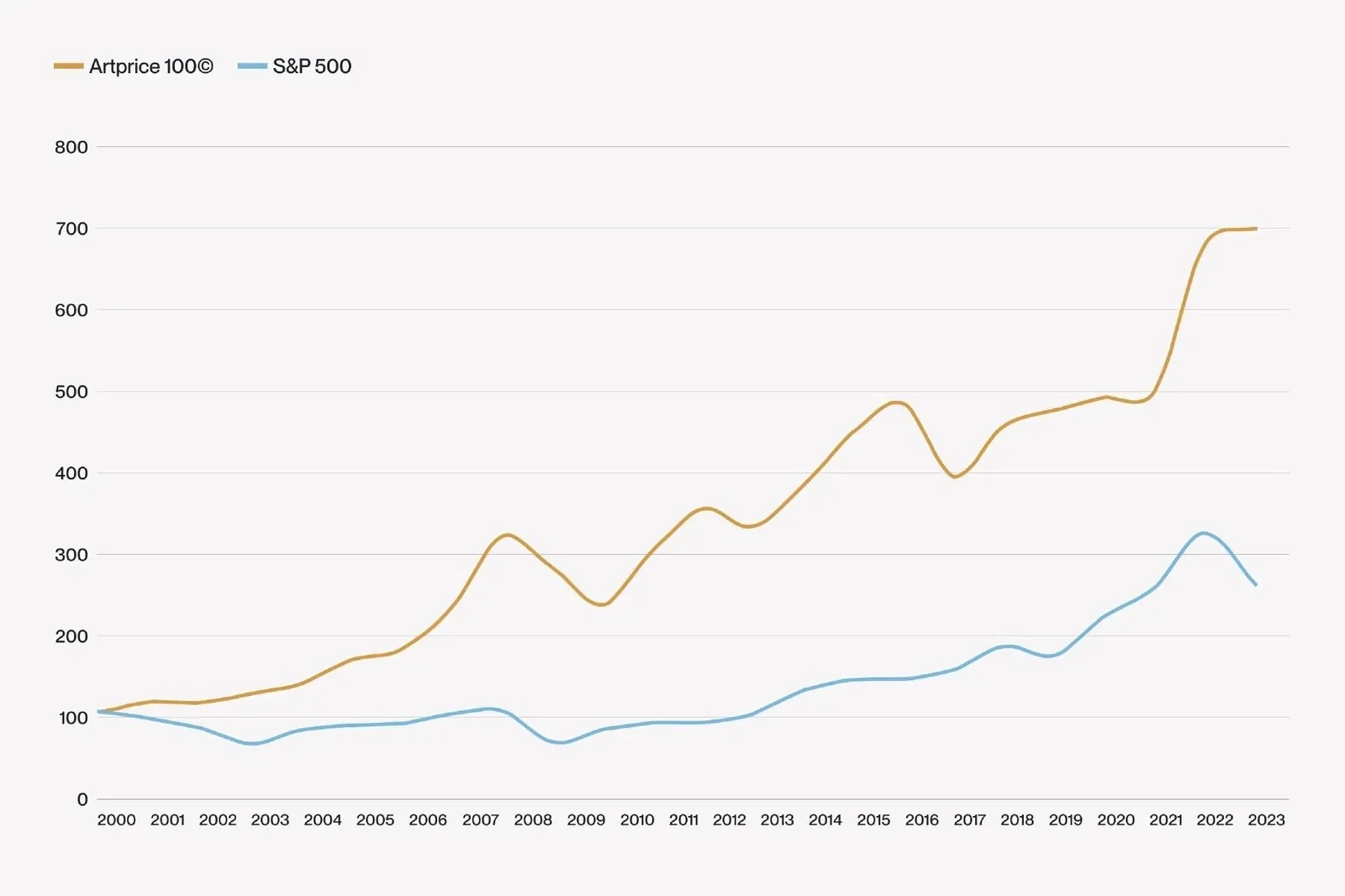

Launched in 2018 by Artprice, the leading art market data provider, the Artprice100 aims to be exactly what the S&P 500 is for stocks. It tracks the one hundred most important artists in the global art market, creating what we might call a "blue-chip art index."

Here's how it works conceptually. Imagine you had invested one hundred dollars evenly across these one hundred major artists back in January 2000. The index tracks what that hypothetical portfolio would be worth today based on actual auction results for these artists' works. The artists selected are those with consistently high auction results over the preceding five years, and each artist's weight in the index corresponds to their auction turnover. This means Picasso, who sells frequently and at high prices, has more influence on the index than a less-traded artist.

What makes this particularly valuable is the careful curation. A scientific committee reviews the composition annually, removing artists whose market has weakened and adding emerging stars, much like how the S&P 500 committee adjusts its constituents. This keeps the index representative of the market's top tier rather than becoming a museum of past glories.

The performance has been remarkable. Over eighteen years from 2000 to 2018, the index's value multiplied by approximately 4.6 times, representing a 360% gain or roughly 9% average annual return. According to Artprice, this outpaced both the global art market index and the S&P 500 over the same period. More recently, the index has shown an average annual return near 10% since 2000, though individual years vary considerably. In 2023, for instance, during a quieter market period, the return was just 1.55%.

What this tells us is something important about market structure. The highest quality works by established masters tend to be more stable and often appreciate even when the broader market stumbles. This is the "masterpiece effect" you'll hear experts discuss—the best pieces outperform the average, creating widening price gaps over time.

For Moon Above and our clients, the Artprice100 serves as a benchmark for evaluating high-end art investment performance. It helps answer the question: "Is my collection of blue-chip works keeping pace with the market for similar quality pieces?" However, and this is crucial to understand, this index doesn't capture emerging artists or the full market spectrum. It's specifically designed to measure the stable, liquid top tier.

The Artprice Global Index: Seeing the Whole Picture

While the Artprice100 focuses on excellence, the Artprice Global Index casts a much wider net, encompassing all auction sales across all artist categories worldwide. Using a methodology called "repeat sales regression"—which tracks how prices change when the same or similar works are resold—this index attempts to measure the entire art market's direction.

The results tell a different story than the blue-chip index. Over its first twenty years, the global index rose only about 30%, according to Artprice founder Thierry Ehrmann. If we set it at 100 in the year 2000, it would reach approximately 130 twenty years later. That's modest growth compared to the Artprice100's trajectory, and there's an important lesson here.

When you include every artist—from museum-quality masters to regional painters to declining reputations—you capture a much more moderate growth rate. Many artists' markets stagnate or even decline over time. The global index shows us the reality that not all art appreciates, and in fact, the average performance across all art is fairly modest. This broader view is essential because it prevents us from being seduced by only looking at success stories.

The global index excels at showing us major market cycles affecting the entire art world. Through it, we can identify the rapid expansion of the mid-2000s, the sharp 2008-2009 crisis correction, the adjustment period of 2015-2016, and the post-2020 recovery. These macro trends affect all segments to varying degrees, and understanding them helps with timing and risk management.

Individual Artist Indices: Tracking Specific Careers

Now let's zoom in further to individual artist tracking. Both Artprice and Artnet offer tools that create indices for specific artists, essentially answering the question: "How has this particular artist's market performed over time?"

These are calculated using either repeat sales data when available or hedonic regression models that adjust for the characteristics of different works to estimate an average price trend. The result is typically presented as a curve or index starting from a base value of 100 at some reference date, showing the artist's appreciation or depreciation.

Let me give you a powerful example of what these reveal. The contemporary artist Christopher Wool's price index, starting at 100 in the year 2000, multiplied by nearly thirty times by 2016. That's extraordinary appreciation. But here's what makes this more than just a number: when you examine what happened in Wool's career during this period, the index tells a story. He gained representation by top galleries like Gagosian and Simon Lee, had major solo exhibitions across Europe, and achieved consecration with a Guggenheim Museum retrospective. The price curve essentially maps his journey from respected artist to market phenomenon.

This illustrates something vital about using artist indices properly. They shouldn't be read in isolation but rather in conversation with the artist's career trajectory. Major gallery representation, museum exhibitions, biennale participation, scholarly monographs—these are the events that drive the curves upward. An expert like Jean Minguet from Artprice emphasizes this point: you must contextualize price indices with career milestones to truly understand what's happening.

For investors, individual artist indices help identify where an artist sits in their market cycle. Is their price at an all-time high after a speculative bubble? In recovery after hitting bottom? Stagnant for years? This temporal context informs buy and sell decisions. However, use these carefully. Artist indices based on small sales volumes can be volatile—one auction record or a dry spell without sales can swing the index dramatically without representing a true trend. Different data providers may also use varying methodologies, introducing inconsistencies.

Sectoral Indices: Mapping the Market's Geography

Beyond tracking individual artists, indices can map entire market segments, giving us a geographical understanding of where opportunities and risks lie. Let me explain the three main ways we slice the market.

By Period and Movement

The art market traditionally divides into major historical periods: Old Masters (ancient art through roughly the eighteenth century), Nineteenth Century Art, Modern Art (late nineteenth through mid-twentieth century, including Impressionism), Post-War Art (post-1945 through the 1970s), and Contemporary Art (recent decades, often defined as artists born after 1945 or 1950).

Each period has its own performance trajectory, and the differences are striking. Over the past quarter century, Post-War and Contemporary art have dramatically outperformed older periods. This isn't surprising when you think about it. Contemporary artists were building their reputations and market presence during this time, creating growth opportunities. Meanwhile, the greatest Old Masters works already reside in museums or permanent collections, making them rare at auction and limiting market dynamism.

Data from Artnet analyzed by private banks shows that Old Masters and Impressionist art had essentially zero returns over fifteen years, while Post-War and Contemporary segments achieved annual growth rates of 7-8% during the same period. This divergence appears even within the Artprice100 composition: in 2023, about 43% of the virtual investment fell within Modern Art, while Old Masters were almost entirely absent due to insufficient auction volume.

What drives this? Contemporary art benefits from abundant supply—living or recently deceased artists continuously create new work. There's a vibrant primary market through galleries, constant media attention, and new wealthy collectors from Asia and the Middle East entering the market. The 2017 sale of a Basquiat painting for $110 million to a Japanese collector exemplifies how new demand drivers have propelled contemporary art prices.

For investment strategy, period indices are crucial for portfolio allocation. Old Masters offer stability with minimal growth—a conservative holding. Contemporary art offers higher potential appreciation but with greater risk and volatility. The indices quantify these differences, helping investors balance established segments against emerging opportunities based on their risk tolerance.

By Medium and Category

Another critical segmentation is by artwork type: Painting, Works on Paper (drawings, watercolors), Sculpture, Photography, and Prints and Multiples. Each medium has distinct market dynamics and therefore different performance patterns.

Painting traditionally dominates fine art auction value, attracting the broadest collector base. Photography, as a relative newcomer to the collecting world, experienced rapid growth during the 2000s as demand exploded, then matured. Sculpture markets can be highly volatile because pieces are often unique or in very limited editions, meaning one record sale can spike an index dramatically.

Prints and Multiples represent a separate category often excluded from fine art indices because they're editions rather than unique works. However, tracking this segment reveals important information about artist accessibility. The explosion of signed editions by artists like Banksy or Yayoi Kusama has massively increased trading volume while potentially diluting their average price growth.

Medium indices help investors fine-tune allocation strategies. If painting indices show prices at historical peaks while photography indices indicate a correction has occurred, that might suggest photography offers better value entry points at that moment. It's about finding relative value across different types of artwork.

By Geography and Regional Markets

The art market, though global, exhibits strong regional patterns. Geographical indices track either where sales occur (auctions in different countries) or the origin of artists being sold (European artists versus Asian artists, for example).

The geographical shift over recent decades has been dramatic. In 2006, China represented only about 5% of the global market. By 2011, it had briefly surpassed the United States, and it has remained in the top three ever since. By 2016, Asia's share of global auction sales reached 40.5%, exceeding both Europe at 31% and the Americas at 27.5%. More recently, the United States has maintained the number one position globally at 39% of market value, with China at 18.4% now nearly tied with Europe's 18.5% for second place.

These regional indices reveal major market shifts and growth opportunities. An investor tracking these trends in the 2000s might have identified the Asian market boom early and positioned accordingly, perhaps acquiring Asian artists or participating in Hong Kong and Shanghai auctions to capture that growth.

Regional indices also capture local economic impacts. A UK market index might reflect Brexit effects on London sales, while a Middle Eastern index could track the rise of Dubai and Doha as art centers with new museums and local wealth. The 2016 TEFAF report noted that while US auction sales plunged 41% in value, Chinese sales dropped only 1.6%, signaling Asian market resilience during an American correction.

For international diversification, geographical indices serve as navigation tools, helping investors rebalance exposure between regions based on relative performance and outlook, much as one might shift between different national stock markets.

The TEFAF Art Market Report: The Macro View

While quantitative indices from Artprice and Artnet provide the numerical foundation, the TEFAF Art Market Report offers something equally valuable: comprehensive qualitative analysis and broader market statistics.

Published annually by The European Fine Art Foundation to coincide with TEFAF Maastricht fair, this report stands apart by attempting to measure the total art market, not just public auctions. It estimates both auction sales and private sales through galleries, dealers, and private transactions between collectors. This matters enormously because private sales often exceed public auction volume.

For example, TEFAF's 2017 report estimated the global art and antiques market at $45 billion in 2016, up 1.7% from 2015. Within this, public auctions accounted for approximately $17 billion (down 19% from 2015), while private sales through galleries and brokers made up more than half the total. This revealed something crucial: despite falling auction numbers, the overall market remained stable because activity had shifted to private channels. Indices based solely on auction data would have suggested a declining market, when in reality, transactions had simply moved out of public view.

The TEFAF report enriches our understanding in several ways. It profiles market participants by region, tracking shares held by the United States, Europe, Asia, and the Middle East, and documenting the rise of new wealthy collectors. In 2022, for instance, the US and China each held roughly 33-34% of the global market, with Europe around 22%, showing the shifting center of gravity eastward.

The report also examines generational changes among collectors. A special "Online Focus" edition noted that 57% of Americans aged 25-34 felt comfortable buying art online, signaling both demographic renewal and digital transformation. This kind of behavioral data helps anticipate future market evolution—younger collectors may favor different artists and purchasing channels than their predecessors.

Digital transformation receives particular attention in TEFAF reports. The 2017 Online Focus revealed that 64% of surveyed galleries already sold online, and approximately 8% of global auction value occurred via internet bidding. However, online sales represented only 4% of gallery revenue in 2016, showing that traditional models still dominated. These metrics track the art world's digital adoption, accelerated dramatically by the 2020 pandemic when Christie's and Sotheby's reported record online sales.

The report also compares public auctions versus private sales channels, quantifying the growth of private sales at major houses. In 2016, Christie's conducted roughly $940 million in private sales beyond its auctions. This highlights the importance of the off-market sector that indices don't capture. Similarly, TEFAF documents art fair growth—attendance, number of fairs, percentage of gallery revenue generated at fairs—showing how sales increasingly occur at international fairs rather than traditional auction houses.

For Moon Above's strategic planning, TEFAF provides the macro context within which we operate. It answers questions about overall market size and health, identifies growing segments and regions, and reveals structural changes like digitalization or market concentration around mega-galleries and auction houses. We can use these insights to adjust our approach—perhaps emphasizing Asian market connections if data shows capital flowing there, or recognizing saturation in ultra-high-end segments and focusing on mid-tier opportunities instead.

Other complementary sources like the Art Basel & UBS Report and Deloitte Art & Finance studies provide additional annual data. The key for Moon Above is aggregating these knowledge sources to maintain the most complete 360-degree market view possible.

How Moon Above Applies These Insights Strategically

Let me now explain concretely how we at Moon Above use these indices and market data to guide our strategy and serve our clients.

Building Data-Driven Art Portfolios

Moon Above applies portfolio management principles borrowed from finance to art collecting. Based on historical index performance, we can define target allocations across market segments. For instance, analysis might suggest allocating 50% of budget toward established blue-chip artists (providing the value foundation, following the Artprice100 or equivalent), 30% toward fast-growing international contemporary art (identified through Contemporary Art indices, boosting potential returns), and 20% toward specialized or emerging niches (young ultra-contemporary artists, digital art) for diversification and hoped-for outperformance.

This allocation isn't rigid—we adapt it to each client's profile—but it illustrates how we use indices to rationally weight an art portfolio. Concretely, if indices signal a segment is overheating (say urban art has risen X% annually for five years), we might limit client exposure to avoid buying at peak prices. Conversely, if a sector index shows relative undervaluation (perhaps design or photography in a cyclical trough), we might see a contrarian investment opportunity.

This data-driven approach makes collection building more objective, aiming to optimize the return-risk balance in art while respecting the collector's artistic preferences. It's about bringing financial discipline to what has traditionally been purely intuitive decision-making.

Index-Driven Positioning and Differentiation

Moon Above distinguishes itself from traditional art advisors through our index-centered, data-focused positioning. Every purchase or sale recommendation rests not only on expert opinion about artistic quality, authenticity, and provenance, but also on quantitative market analysis of that artist or segment.

This hybrid approach offers competitive advantages. It reassures investors by objectifying recommendations—for example, showing that a work is trading 20% below its average recent auction price according to indices, suggesting good value. It brings transparency to market trends. Being "index-driven" means we can benchmark a client's collection performance against market indices at any time, much as a wealth manager would evaluate a stock portfolio against the CAC 40 or S&P 500.

This pedagogical approach helps clients understand their collection's value evolution using modern tools. It's an innovative positioning in an art world that often remains opaque. Moon Above positions itself at the forefront of data-driven art advisory, without neglecting connoisseurship—the trained eye remains essential for judging an artwork's intrinsic quality.

Editorial Analysis and Enriched Content

Index exploitation doesn't just serve portfolio management—it fuels Moon Above's editorial content. As a research-oriented platform focused on knowledge sharing, we regularly publish articles, studies, and insights on the art market, much like this piece you're reading now.

Indices provide the factual foundation for comparisons and deep-dive studies. We might leverage historical data to compare contemporary art performance versus stock markets over twenty years, numbers in hand, creating educational content for investor readers. Geographical indices enable regional focuses: analyzing China's market rise since 2000 by showing how Chinese artist indices have exploded, or examining the emerging Middle Eastern market.

Other content ideas include historical analysis (perhaps examining tulip mania and parallels with art speculation bubbles), sectoral studies (has sculpture underperformed painting over fifty years?), or artist performance rankings (top ten artists with greatest value appreciation over the past decade according to indices).

This analytical content, enabled by index mastery, reinforces Moon Above's authority and offers our community deep art market knowledge. It's also a means of financial education for collectors, aligned with Moon Above's mission to democratize informed art investment.

Important Limitations and Necessary Caution

Despite their substantial value, art market indices have limitations that require careful interpretation alongside human expertise. Let me walk through the main precautions you should keep in mind.

Partial Data and Coverage Bias

Most indices rely exclusively on public auction results because these are the most accessible and verifiable data. However, the total art market includes a vast primary market (direct artist sales through galleries) and numerous undisclosed private sales. These non-transparent segments often represent more than half of the art market's actual total turnover.

Consequently, an auction-based index may neglect significant activity. If buyers shift from public sales toward private transactions, as happens in certain cycles, the auction index will decline even while private prices remain stable. Similarly, global indices may over-represent highly active auction regions like China and the US while underestimating quieter markets.

This doesn't prevent indices from being good thermometers of general trends, but their movements sometimes need nuancing with knowledge of behind-the-scenes activity—gallery sales, post-auction private sales, and so forth.

Temporal Lag

Art indices aren't real-time indicators. They're typically calculated quarterly or annually, based on sales that occurred weeks or months earlier. This creates an information lag. An annual 2023 index won't deliver its verdict until year-end, even if the market began shifting trajectory mid-year.

When shocks occur—economic crises, geopolitical events—we must await subsequent auctions to see effects reflected in indices. Indices don't predict the future; they document the recent past. Thus investors shouldn't rely on them solely for anticipation—they primarily confirm trends after the fact.

At Moon Above, we complement index analysis with continuous qualitative monitoring to detect early signals before quarterly indices reflect them.

Illiquidity and Realization Constraints

Unlike a stock index you can invest in via an ETF with a few clicks, an art index isn't directly investible. Replicating an index's performance would require purchasing the underlying works (or a sample) in the same proportions—practically impossible.

The art market is inherently illiquid. Each work is unique, sale opportunities depend on owner willingness, and transaction costs are substantial (auction commissions, insurance, transport). An index might show a 10% gain, but this doesn't guarantee an average collector could actually have resold their paintings with 10% profit in that period—they might not even have found buyers quickly.

Index performance should be viewed as theoretical benchmarks. Moreover, indices generally don't account for fees and delays. On physical objects like art, these are far from negligible—between gallery or auction house margins and taxes, prices often must rise significantly just to cover costs.

Art lacks stocks' liquidity, which should temper enthusiasm aroused by beautiful ascending index charts.

Superstar Effect and Survivorship Bias

The art market follows a superstar economy where a few artist-celebrities capture most value. Estimates suggest a tiny fraction of artists (1% or less) represent the majority of annual sales value. This means global indices can be heavily influenced by results from these few stars—Picasso, Warhol, Monet.

When one superstar's prices soar, it pulls the index upward, creating the illusion that "the art market" broadly is booming, when most lesser-known artists may not be following this trajectory. An economist noted in 2017 that "the superstar phenomenon is omnipresent in the art market: a very small number of artists generates most sales."

Investors must remember that an index's average performance doesn't reflect the median artwork's performance. In reality, many artists' markets stagnate or progress modestly while a few explode and lift the average.

Similarly, several indices suffer from survivorship bias. Their composition is regularly adjusted—"losing" artists exit the index, replaced by new trending entrants. This tends to maintain the index's historical performance through retrospective filtering. Journalist Felix Salmon critiqued Artnet's C50 (Contemporary 50) index, showing its strong historical performance stemmed from incorporating contemporary artists after they became stars—something no investor could have predicted in advance. In other words, "if you only retained things that worked extremely well, you'd get terrific returns—thanks very much."

Indices tend to overestimate what a realistic investor could have achieved because they abstract from failures (artists fallen into obscurity, unsold works) and overweight successes. Prudence dictates using indices as trend indicators and comparison tools, not as guarantees of future gains. Each art acquisition must be analyzed individually, indices in hand, to evaluate its specific potential.

Moon Above's Positioning: Index-Driven Art Investment Advisory

To conclude, Moon Above promotes an approach to art investment founded on an unprecedented alliance between financial data and curatorial interpretation. Our positioning can be summarized as "index-driven art investment advisory"—investment counsel guided by indices. Concretely, this means we use all available quantitative market indicators (price indices, annual reports, macro and micro data) to inform every decision, while integrating the artistic and cultural dimension indispensable for evaluating an artwork.

This hybrid approach offers the best of both worlds. On one hand, data rigor—comparable to that mobilized by traditional financial advisors—bringing objectivity and transparency. On the other hand, the connoisseur's sensitivity—because investing in art cannot be reduced to numbers alone; you must also understand the history, rarity, and aesthetic quality of works. Moon Above positions itself as a bridge between finance and art, where statistical analysis illuminates the passion of collecting.

Being "index-driven" means every client recommendation will be supported by tangible market elements. We can show, for instance, that a particular work belongs to a segment growing 5% annually over ten years, that the artist outperforms their movement's index, or that selling timing is favorable because the global market index approaches a historical peak. Simultaneously, our team brings curatorial expertise to judge whether the work possesses the artistic qualities and adequate provenance to meet long-term value criteria.

This "data plus expertise" positioning allows us to offer holistic counsel, combining reason and passion. Moon Above aims to be a trusted partner for cultivated collector-investors who aren't specialists, desiring to approach the art market with the same analytical tools used for other wealth investments, while preserving the pleasure and intellectual richness inherent to art.

Our credo—"index-driven art investment advisory"—reflects the ambition of a new generation of art counsel, where decisions are illuminated by both market indices and informed human judgment. In this spirit, we accompany our clients so that art investment combines financial performance with cultural fulfillment, confidently and successfully.

At Moon Above, we believe that understanding the tools of art market analysis empowers collectors to make better decisions. Indices aren't crystal balls, but they are powerful lenses that help us see patterns, identify opportunities, and manage risk in what has historically been an opaque market. By combining this quantitative foundation with deep artistic expertise, we help our clients build collections that satisfy both their aesthetic passions and their financial objectives.